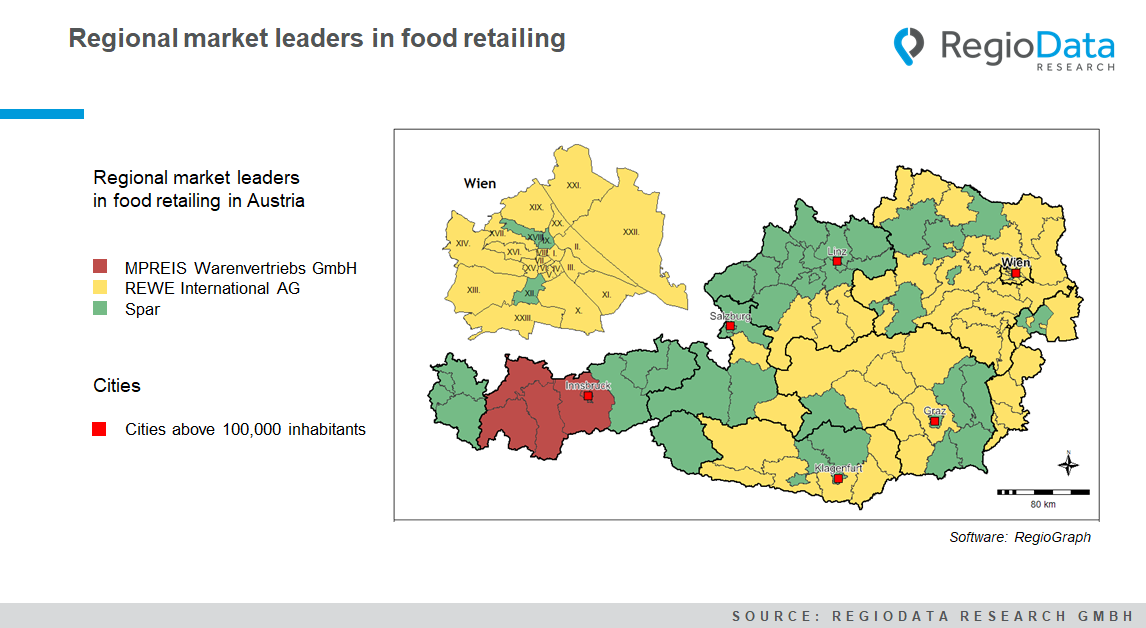

The small-scale representation of the market leaders in Austrian food retailing illustrates the initial origins of the companies:

While REWE (with Billa) has its roots in the federal capital and was able to expand its market leadership in Vienna and the whole of eastern Austria at an early stage, Spar with its roots in Tyrol and Salzburg remains well established, especially in the west. In terms of sales area, however, the rivals are close together: In food retailing, REWE can still claim first place with a total sales area of around 1,211,000 m2, although the Spar Group is on the heels of its main competitor with around 1,135,600 m2 of sales area.

For several decades, both companies have been trying to expand their sphere of influence: REWE in the direction of the West and Spar in the East – but all in all with mediocre success.

With a good 467,400m2 of sales area, the third major market player in Austria, Hofer, is no market leader in any region, and neither is Lidl, but this is also due to the discount store type. The discount store type only has a combined market share of barely under 30% in Austria.

In the west, however, the situation is much more differentiated: In Vorarlberg, Sutterlüty – an independent company with a significant shareholding by REWE – plays an important role. And in Tyrol, M-Preis is the local hero, but was originally only able to extend its market leadership from the Innsbruck area westward to the Arlberg.

With a total sales area of 3,340,718 m2 in the food retail sector throughout Austria, the people of Graz eat up more sales area than in any other district. The title for the district with the highest sales area thus goes to Graz at around 106,680 m2. The area with the lowest commercial space is in Rust Stadt measuring just 950 m2.